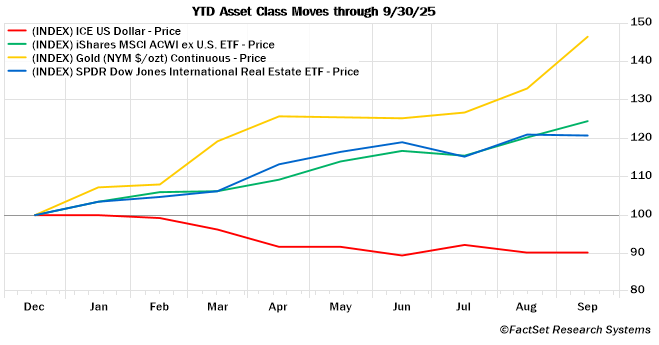

The U.S. dollar (USD) has experienced a historically bad year. Its return through the first half of the year was the worst in over 50 years. Through the third quarter, the USD was down 10% year-to-date. The ramifications of this weakness have rippled across asset classes. Foreign equities, foreign real estate, and precious metals are among the assets that have registered historically good years.

What forces are driving the USD? How might these influence portfolio positioning?

U.S. Dollar Cycles

As shown above, the USD has experienced multiple major cycles over the last 50 years. While each cycle has its own unique characteristics, a few common forces underpin the cycles: relative growth, relative interest rates, and relative quality. These forces are at play in 2025, too.

Relative Growth

Periods of strong U.S. growth relative to the rest of the world have attracted demand for the USD, supporting its value. This was seen in the late 1990s, after the Global Financial Crisis, and following COVID. Shifts in relative growth rates, however, can shift relative demand for currencies.

The Eurozone and the United States together provide a good illustration. This is because when USD performance is cited, it is relative to a basket of currencies, by far the largest of which is the Euro. FactSet estimates that in 2025, the Eurozone’s real GDP growth accelerated while the U.S. decelerated, improving the Eurozone’s relative growth rate from -2.3% in 2023 through 2024 to -0.5%. This improving relative growth has helped the Euro appreciate over 13% vs the USD year-to-date.

Source: FactSet

Going forward, a key variable for relative U.S. real GDP growth is productivity. USD strength starting in the mid-1990s was catalyzed in part due to an inflection in U.S. productivity from technology investment. While the lag between technology investment and productivity gain has varied over time (shorter in the 1990s, longer in the 1970s and 1980s), AI-related investments offer the potential for productivity improvement over the next few years.

Relative Interest Rates

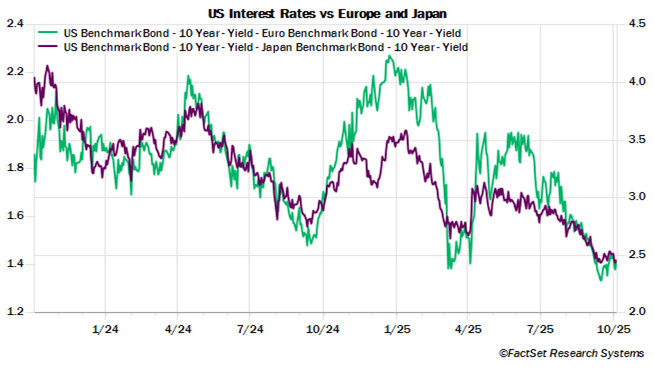

The Federal Reserve was able to raise rates earlier than global peers coming out of COVID and executed a cutting cycle slower than global peers. This helped support relative interest rates in the United States, attracting demand for the USD. A moderating employment backdrop has led the United States Treasury market to anticipate a faster rate cutting cycle, just as global peers have begun to pause their cutting cycles. The 10-year Treasury yield premium the United States has offered relative to other developed markets has dipped, making the USD less compelling.

In the future, lower United States interest rates may support cyclical parts of the economy that have struggled under higher interest rates like housing and non-residential real estate. If these areas were to pick up, it could boost the relative growth of the United States. A more resilient labor market and a continued easing of tariff-related inflation pressures could allow the Federal Reserve to avoid cutting rates as much as expected, supporting relative interest rates and buttressing the USD.

Relative Quality

The United States financial markets are the deepest and most liquid in the world. The United States has led increased globalization for decades. Compared to other developed countries, debt-to-GDP ratios were contained. Compared to emerging countries, institutions were stable. Strong United States relative growth and rates combined with these quality traits meant foreign investors, who hold over $60 trillion of U.S. assets, did not feel the need to hedge their USD exposure at high levels. After all, the USD was a safe haven. 2025 has incentivized more hedging and diversification away from the USD because not only have relative growth and interest rates declined, but the quality traits the United States was known for have come into question for some investors.

Some variables are arguably temporary. Trade policy uncertainty is still elevated but improving. The government shutdown is a noisy event that has historically not held material significance for future asset class returns. Corporate bond spreads are tight, indicating the bond market is not worried about either factor impacting risk.

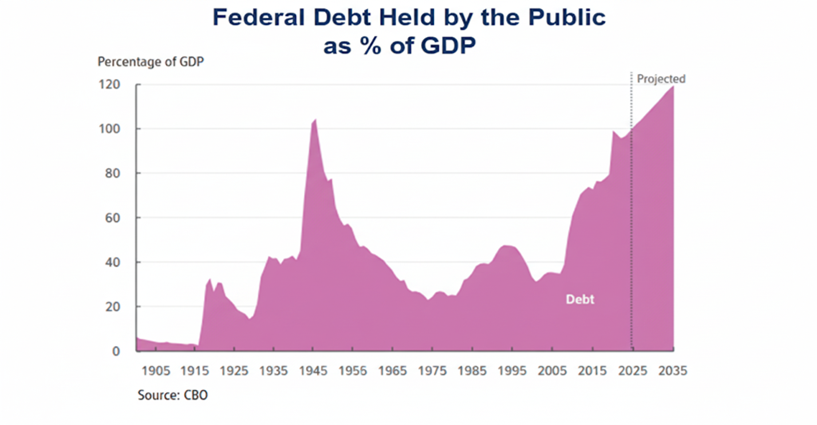

A more structural variable is government debt. Entitlements remain a key issue driving deficit spending and need for higher debt levels.

Maintaining the rule of law and institutional integrity, and calming down the economic policy volatility could support the U.S. dollar.

Portfolio Positioning

When an asset has experienced a historically bad run, it is easy to extrapolate the negativity. That psychological dynamic is the reason for highlighting the ways the USD’s relative growth, interest rates, and quality dynamics may improve. But the Osborne Partners Investment Team’s process is not based on hope or making a call on a macro variable like the direction of the USD. Instead, the focus is on individual asset risk-reward while keeping the overall portfolio’s risk profile in mind. A multi-asset class portfolio enables resilience across scenarios. This is shown by the following asset correlations that capture how two assets perform with one another. A negative correlation means if the USD goes down, the asset tends to go up, and vice versa. Assets that are priced in other currencies, such as foreign assets, or assets that are viewed as alternatives to the USD, such as gold, have the strongest inverse relationship with the USD.

Consistent with longer term correlations, gold (IAU), international real estate (RWX), and foreign equities (ACWX) have performed well as the USD has performed poorly. The Investment Team continuously reassesses the risk-reward of the portfolio and watch list positions as assets are repriced due to macro variables like the USD or asset-specific variables like earnings. This reassessment is not meant to compel overtrading, it is intended to construct a multi-asset class portfolio that is resilient no matter what USD path materializes.