The September Federal Reserve Open Market Committee (FOMC) meeting delivered a widely expected 0.25% rate cut and underscored the deep divisions within the Federal Reserve (“the Fed”) as they transition toward lower policy rates. The new Federal Funds Rate range stands at 4.00%–4.25%. The cut, largely telegraphed to markets since Chairman Powell’s dovish shift in August, was justified as a “risk management cut,” intended to hedge against rising “downside risks to employment” as the labor market continued to soften. However, with inflation metrics still running well above the 2.0% target, there exists a tension among FOMC members. Recall the Fed has a dual mandate: stable prices and maximum employment. At times, the two prongs may come into conflict, and today is one of those times.

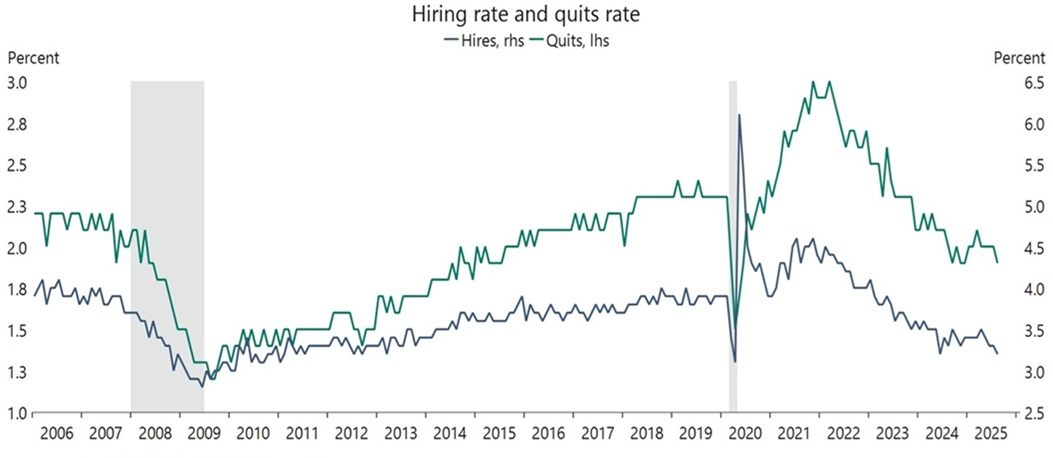

Let’s take a quick look at the numbers. Recent employment growth has slowed significantly. The trailing three-month average job gain slowed to ~30,000 through August. This is down from the recent peak of ~192,000 in January. On top of the ongoing slowdown, the preliminary revision to prior year payrolls (for the year ending March 2025) was revised lower by over 900,000 jobs. There appears to be genuine fragility in the labor markets. Yet, the low demand for workers is presently matched by lower supply of job seekers, converging to form an unusual “low fire / low hire” environment, which Powell referred to as, “a curious kind of balance.”

Source: U.S. Bureau of Labor Statistics, Macrobond, Apollo Chief Economist

Shifting to inflation, the Fed’s preferred gauge (Core PCE) remains elevated at 2.9%. With the impact of tariff announcements not fully settled, and indeed new tariff measures may be introduced still, the risk of reigning inflation to intolerable levels persists. So, the Fed remains deeply conflicted. The current environment forced the FOMC into a compromise. That is, to accept a 0.25% rate cut today to preempt further labor market weakness, while buying two more months of data before deciding what comes next at the subsequent meeting in October.

There was one other wrinkle to the September meeting: the FOMC welcomed its newest voting member to the table. Newly confirmed Fed Governor Stephan Miran, former (and still current?) Chairman of the Council of Economic Advisors for President Trump, cast the lone dissenting vote at the meeting, advocating for a more aggressive 0.50% rate reduction. This reflects his well-known view that current policy is far too restrictive and risks a Fed-induced economic downturn. His quite outspoken opposition highlights the growing political scrutiny toward the Fed. The present situation surely feels like a curious kind of balance.

Other Items of Interest

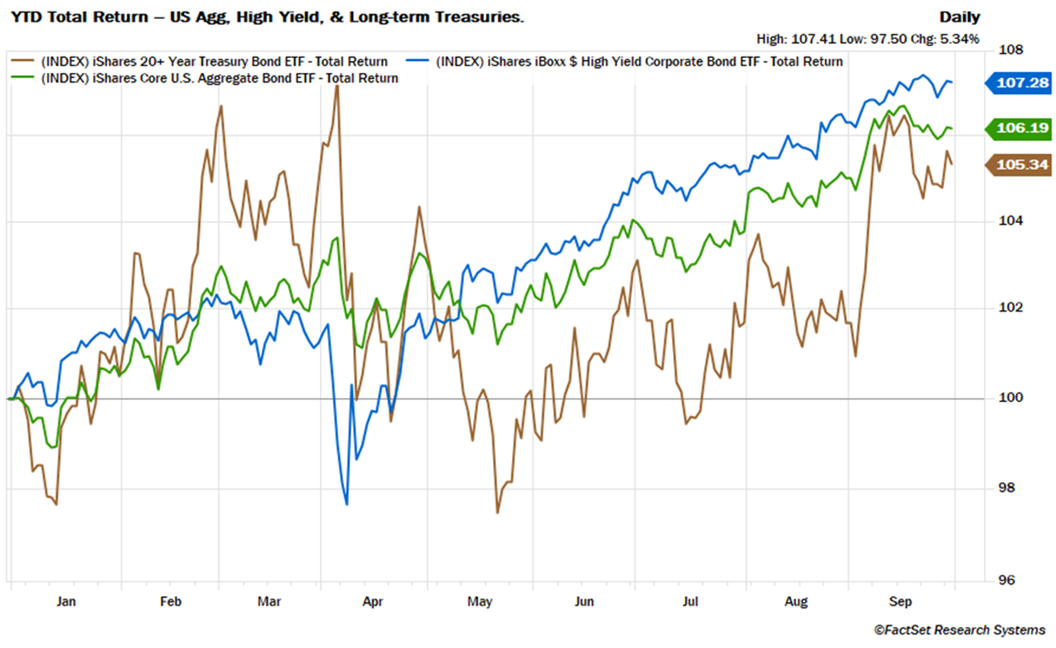

Year-to-Date Performance

Through the end of the third quarter, fixed income performance (on a total return basis) remained very solid. Performance was led by high yield corporate bonds, followed closely by the U.S. Aggregate Bond Index, with long-term Treasuries lagging albeit still solidly positive on the year.

September FOMC Dot Plot

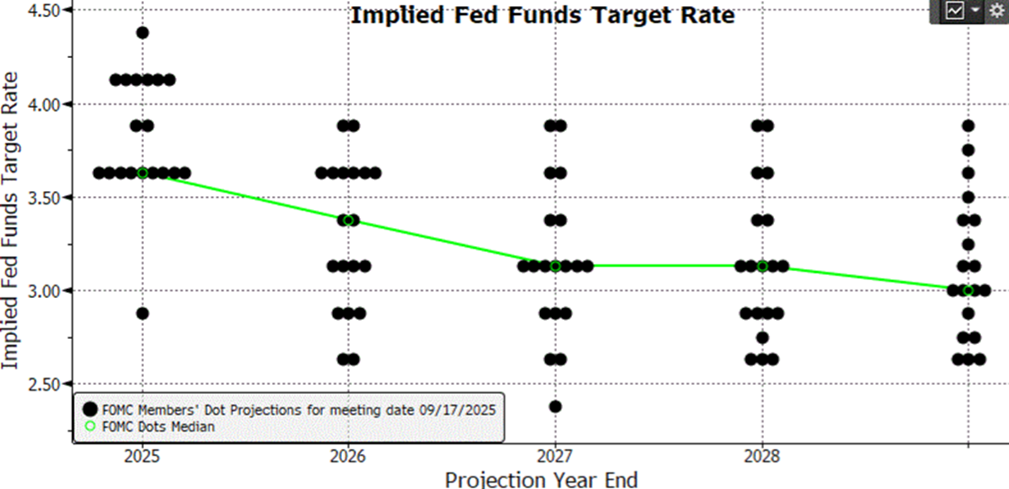

The updated Dot Plot is interesting. Bottom line: it presents only a marginal change to prior forecasts. The new Plot added one new rate cut in 2025 (for a total of three this year), but after adjusting for the additional cut, there was no change to future years. Said another way: the FOMC expects the same future rate path but exiting 2025 at a lower level than previously expected.

Perhaps the more interesting takeaway from the Dot Plot is just how divided members are with respect to near-term policy. The 2025 median Dot was moved lower due to just one individual’s forecast. In fact, one member penciled in six rate cuts for 2025 while another sees a rate hike by the end of the year. Our bold prediction: At least one person is going to be very wrong.

Source: FOMC, Bloomberg

Fed Funds Futures Pricing

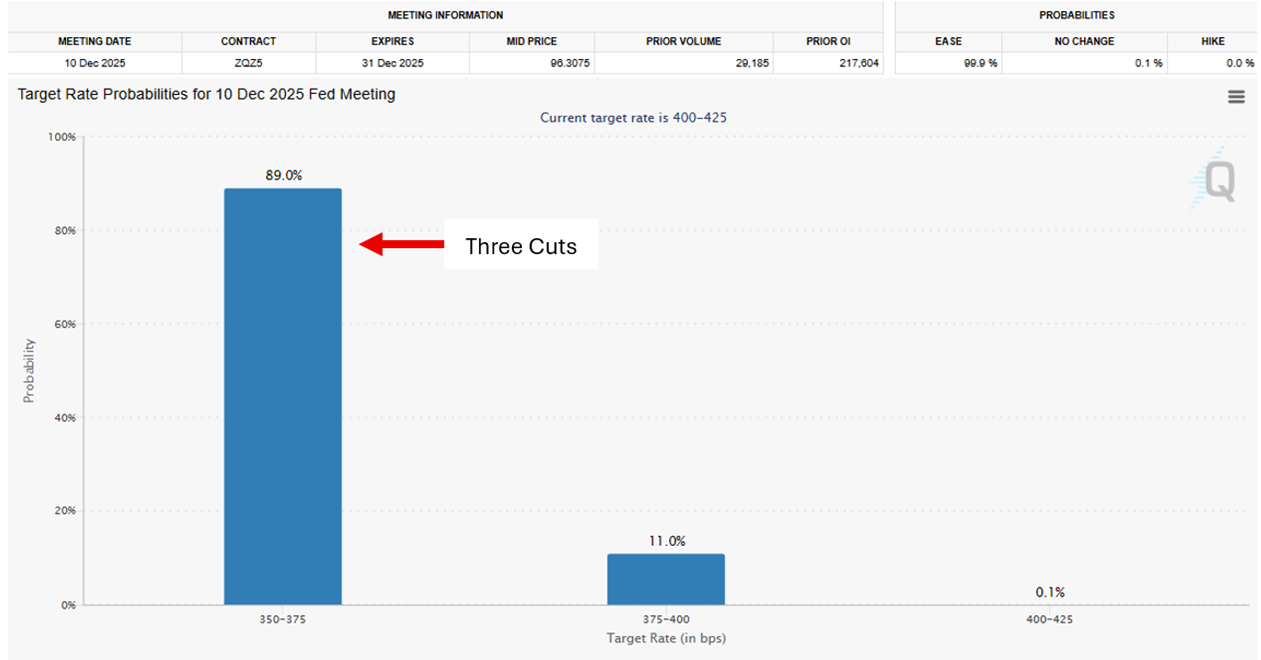

Three months ago, in the last Wealth Report publication*, we wrote that the market had priced in a 35% probability for two rate cuts and 45% for three by the end of 2025 (with the remaining probability evenly split between one and four cuts). Recall at the time that market pricing was well ahead of the FOMC’s Dot Plot projections. Today, after a series of softer jobs and inflation data, the market now expects an 89% probability for three cuts.

Source: CME Group, as of October 1, 2025

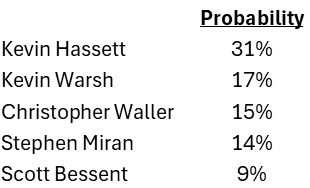

Update on FOMC Chairman Nomination

In the prior Wealth Report*, we highlighted some of the top candidates to replace Jerome Powell as FOMC Chair in 2026. Today, that same group remains at the top of the hypothetical list. Treasury Secretary Bessent is conducting the search (yes, he is also generally considered a top candidate), and has been quoted as saying, “I want to see people who are forward-looking, not backward-looking on regulation,” and someone who “can bring credibility to the markets.” Prediction market snapshot:

Source: Kalshi, as of October 1, 2025