On May 22, 2026, a new era of leadership began at the Federal Reserve. Kevin Warsh succeeded Jerome Powell as the 17th Chair of the Federal Reserve, while Powell remains on the Federal Open Market Committee (FOMC) as a governor. The big question is whether investors can expect the same approach to monetary policy, or whether markets have to adapt to a new way of thinking.

Kevin Warsh Background

Warsh was a Fed governor from 2006–2011, during the global financial crisis. He was one of the youngest Fed governors ever appointed (nominated by George W. Bush) and served as a key liaison to Wall Street during the 2008 crisis. During that period, Fed officials initially dismissed the dangers of the subprime mortgage meltdown before implementing a historic rescue effort that expanded the balance sheet past $4 trillion through quantitative easing — a QE program Warsh argued was too extreme. After leaving in 2011, he became a persistent critic of Fed policy from the outside as a lecturer at Stanford’s business school, and a member of various boards. As recently as last year, he called for “regime change” at the central bank in an interview. He was also a finalist for Fed chair back in 2017 (Trump ultimately selected Powell).

Direct Comparison

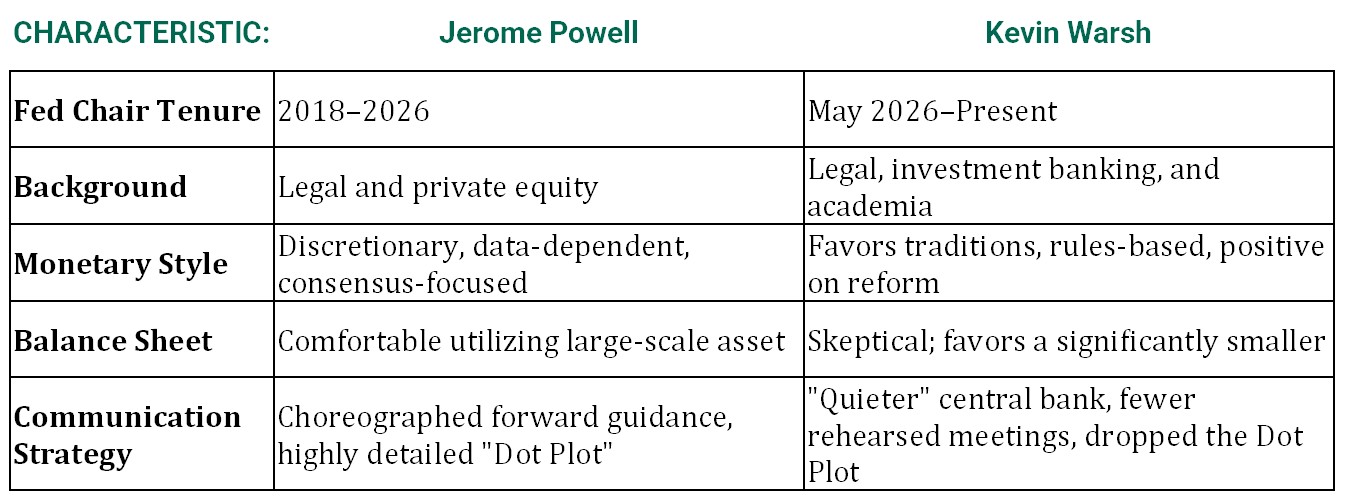

Kevin Warsh and Jerome Powell represent distinct eras of leadership at the Federal Reserve, with Warsh advocating for a rules-based approach that contrasts with Powell’s cautious, consensus-driven tenure. Below are the key distinctions:

Key Similarities

Both Fed Chairs share a background outside of academic economics, as both hold law degrees and worked extensively in private finance.

Both have navigated major financial crises, with Powell leading the pandemic-era response and Warsh serving as Wall Street liaison during the 2008 financial crisis.

Both have faced intense public scrutiny and political pressure from President Trump regarding the direction of interest rates.

Key Differences

Monetary Policy and Balance Sheets

Warsh views massive balance sheets as an “unhelpful” policy tool and advocates aggressively shrinking the Fed’s assets.

Powell leaned heavily on expanding the balance sheet to influence market conditions during economic shocks.

Warsh links long-term inflation dynamics to productivity and government spending rather than just interest rates.

Powell prioritized standard inflation models balancing employment data with core price indexes (PCE).

Communication and Transparency

Powell was highly public and leaned toward consensus-driven transparency by conducting regular post-meeting press conferences.

Warsh favors a quieter central bank, reducing the frequency of scripted public commentary.

Warsh prefers informal meetings with open debate versus pre-choreographed forward guidance.

Inflation

Kevin Warsh views inflation strictly as a “policy choice” that the central bank must eliminate, whereas Jerome Powell approached inflation control more flexibly, favoring long-term trends over reactions to temporary shocks.

Kevin Warsh: Inflation is a “Choice”

Definitive 2% Mandate: Warsh vows that the Fed will unconditionally deliver on its 2% inflation target.

Rejection of Excuses: Despite external supply pressures such as the war in Iran pushing consumer inflation above 4%, Warsh insists that inflation remains a choice determined by monetary policy.

Framework Overhaul: He established a specialized task force to fundamentally review how the Fed analyzes inflation and the sources of economic data.

Hawkish Policy Pivot: As a signal of his stance, Warsh reversed Fed easing by shifting toward a posture that keeps rate hikes heavily on the table.

Jerome Powell: Data-Dependent

We Should Look Through Shocks: Powell advocated that central banks should look through temporary commodity and energy disruptions rather than executing quick interest rate hikes.

Focus on Expectations: He placed greater emphasis on monitoring consumer and market inflation expectations over short-term fluctuations in the Consumer Price Index (CPI).

Dual Mandate Priority: Powell consistently attempted to balance price stability with the labor market, preferring a gradual normalization of rates to avoid damaging employment.

External Noise: Under his tenure, elevated prices were frequently attributed to disruptions and supply chain shocks, justifying a more patient approach to raising rates.

Interest Rates

Kevin Warsh favors keeping interest rates elevated or raising them further to aggressively anchor price stability, directly contrasting with Jerome Powell’s historical preference for cutting rates gradually to protect the labor market. While both agreed to unanimously hold the benchmark interest rate steady at 3.5%–3.75% in June 2026, their philosophies on future rate paths are different.

Kevin Warsh: Hawkish Bias: Despite being appointed by President Trump to lower borrowing costs, Warsh immediately removed language indicating a bias toward future cuts.

Openness to Hikes: Warsh has signaled that interest rates may need to rise further this year to combat resurging inflation.

No Policy Clues: He has not provided an interest-rate forecast to avoid cornering the Fed into a specific rate path.

AI Productivity: Long-term, Warsh believes the AI boom could naturally support lower borrowing costs by improving economic productivity.

Jerome Powell: Balanced Normalization

Preference for Rate Cuts: Before stepping down as Chair, Powell leaned toward easing, leading the Fed to cut interest rates in late 2025.

Dual-Mandate Defense: Powell believes rate levels should tightly reflect a balance between inflation and job market cooling – rapid hikes could threaten employment.

Telegraphed Paths: He leaned on using the “dot plot” to give the public a clear direction of where interest rates were heading.

Current Alignment: Remaining on the board as a governor, Powell voted to hold rates steady alongside Warsh to monitor current economic disruptions.

How Each Prioritize Inflation, Interest Rates, and Employment

Kevin Warsh’s Priorities: Inflation is his top priority. He views interest rates as a policy lever. Employment seems like a secondary item that can be improved with productivity.

Jerome Powell’s Priorities: Inflation is important but should be managed with patience. Interest rates should be a data-dependent tool. The public should not be surprised about the direction of interest rates. Employment was very important to Powell.

Overall, we can expect shorter, more curt, policy statements during and after Fed meetings. We can expect very little to no forward guidance on interest rates. Additionally, besides sounding more hawkish than expected, it will be interesting to see the progress Warsh makes on improving the data presented to the Fed. His goal is to have access to more real-time data. All of this points to the bond market being more important than ever to decipher the direction of interest rates.