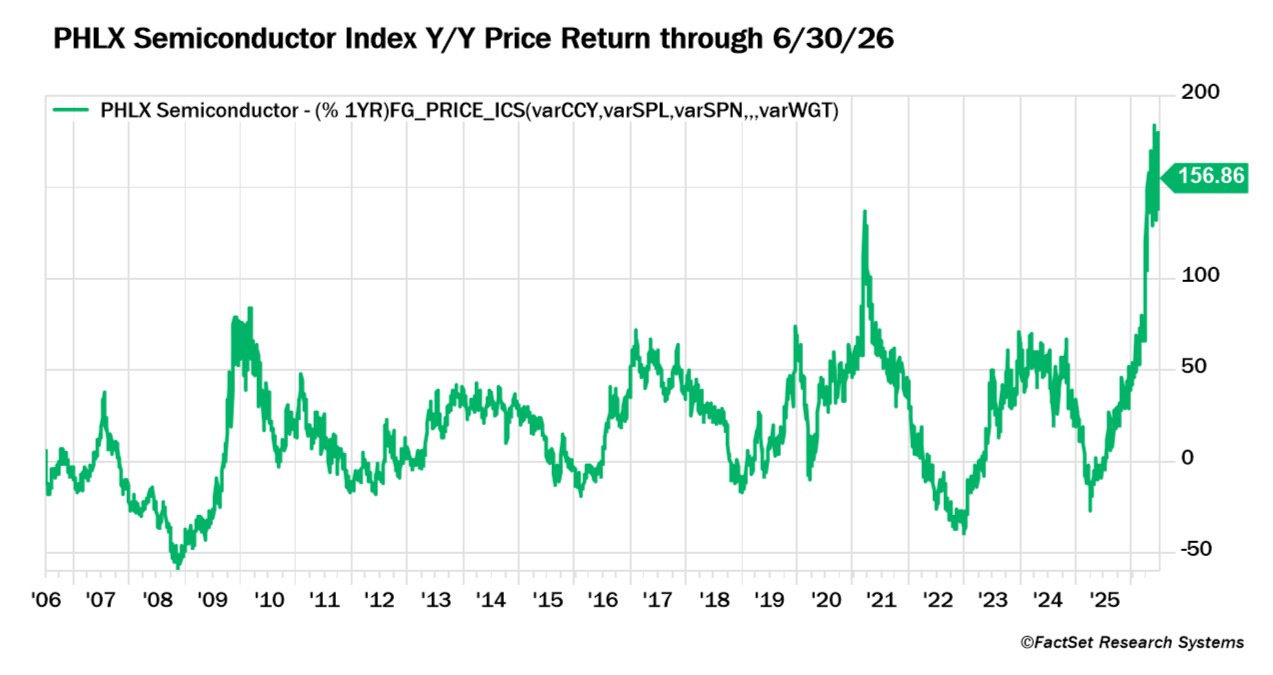

The second quarter of 2026 was filled with records. A semiconductor index had its best quarterly return ever, putting it on pace for the best year since 1999, and leaving the index up 157% year-over-year.

It did not stop there. The biggest ever equity issuance by a US public company was announced. The largest initial public offering (IPO) in US equity market history occurred. Why? The artificial intelligence (AI) investment cycle.

AI Capex

And what a cycle it has become. Per data from the Bureau of Economic Analysis, US tech capital expenditure as a share of US gross domestic product (GDP) is over 4.4%, around the levels seen at the peak of the Dot Com Bubble in 2000. Digging deeper, Goldman Sachs estimates that incremental (i.e., year-over-year) AI capital spending was 0.9% of GDP in 2025 and 1.5% in 2026, close to the peak incremental increases seen at the highs in the late 1990s. Driving these increases are things such as data centers, semiconductors, and networking equipment.

A yellow flag in past capital spending cycles across industries is when companies end up seeing free cash flow (i.e., cash flow from operations minus capital investment) go negative. This necessitates raising liquidity. One avenue is an equity issuance that dilutes existing shareholders. Another route is debt issuance that can increase leverage, and thus risk, if fundamentals deteriorate.

We are now starting to enter the part of the cycle where companies are having to raise liquidity. A group of seven tech companies with large cloud computing infrastructure businesses that are used to support the expansion of AI such as Alphabet, Amazon, CoreWeave, Meta, Microsoft, Nebius, and Oracle has seen a sharp shift in their free cash flow. In 2024, the group generated $230 billion of free cash flow. This year, FactSet estimates they will produce negative $16 billion of free cash flow. All but one of the seven has raised liquidity in 2026.

This cycle has helped buoy companies that are capex beneficiaries such as semiconductors. History, however, has shown that these beneficiaries often start to see moderating returns before capital expenditures moderate.

AI Progress

Such significant investment reflects optimism about AI’s progress. Initially, AI was only generative. Prompt an AI chatbot and get responses. Now AI is becoming more agentic. Assign AI an objective where AI can plan, make decisions, and execute workflows.

At a high level, a few notable forces have influenced this technological shift. Model intelligence continues to scale thanks to advancements in training techniques. Functionality has developed that allows AI models to use various tools. Improvements in database, memory, and retrieval techniques have expanded the models’ information processing capabilities. Creation of orchestration frameworks has allowed multiple types of agents to work on a task concurrently. The engineering of feedback loops has helped models iterate and improve.

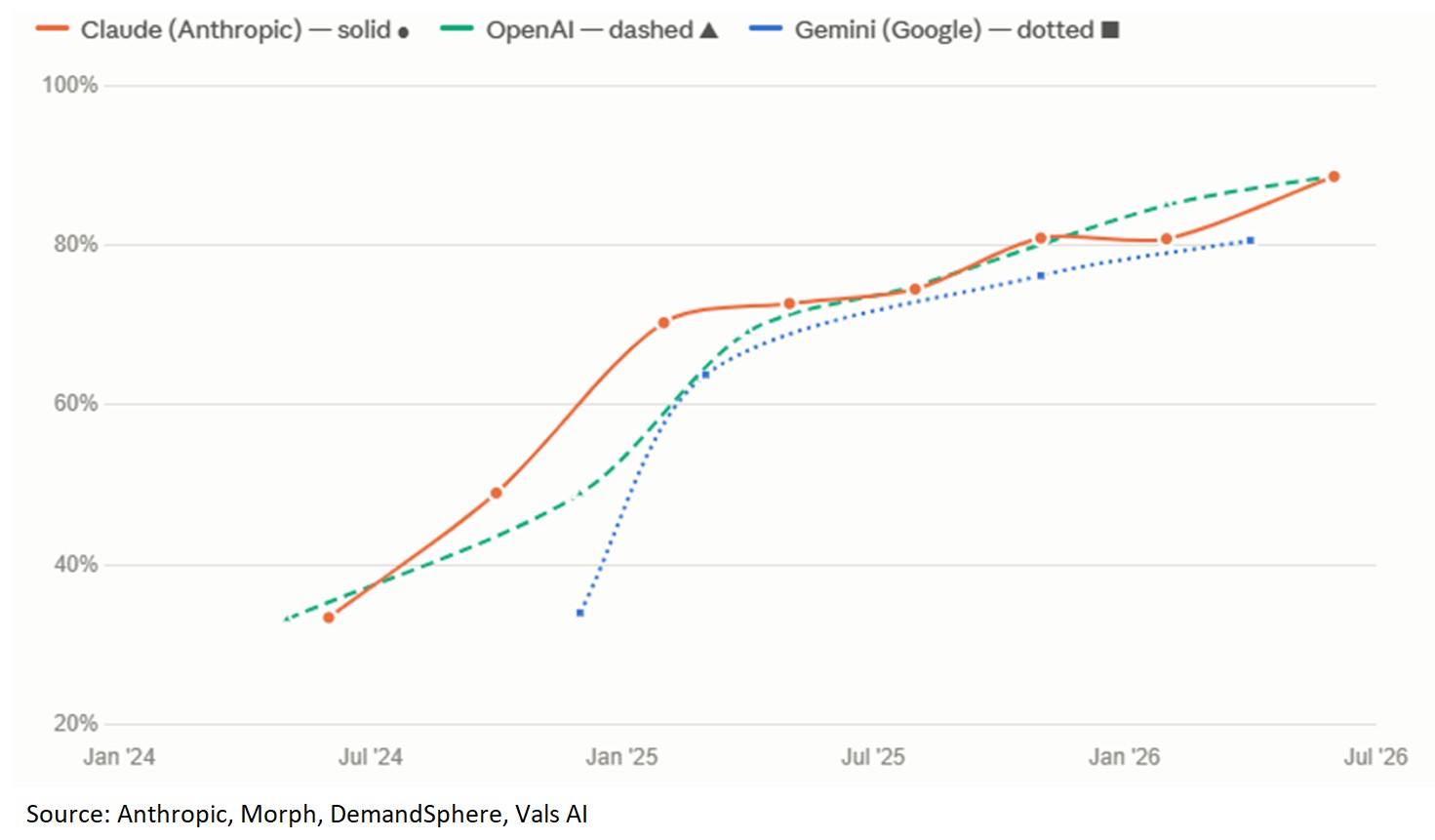

AI model advancement is tracked using benchmarks that attempt to compare the models with human expert performance. Since software engineering coding has exploded as the biggest AI use case so far, led by Anthropic’s Claude Code, consider how leading AI model scores on verified software engineering benchmarks have improved.

Not only have models advanced, the cost to run a model at a fixed level of performance has continued to decline. For example, the estimated blended cost per 1 million tokens (i.e., a token is a basic unit of text, image, or audio that an AI model processes) to use OpenAI’s GPT-4 model in 2023 was $45 versus $7.80 to use GPT-5.2 in early 2026. A few factors have contributed to this. Model developers have made algorithms more computationally efficient. Semiconductor engineers have continued to optimize for processing speed, memory capacity, and bandwidth. Also, open-source model providers, like DeepSeek, have created more competition.

AI Adoption

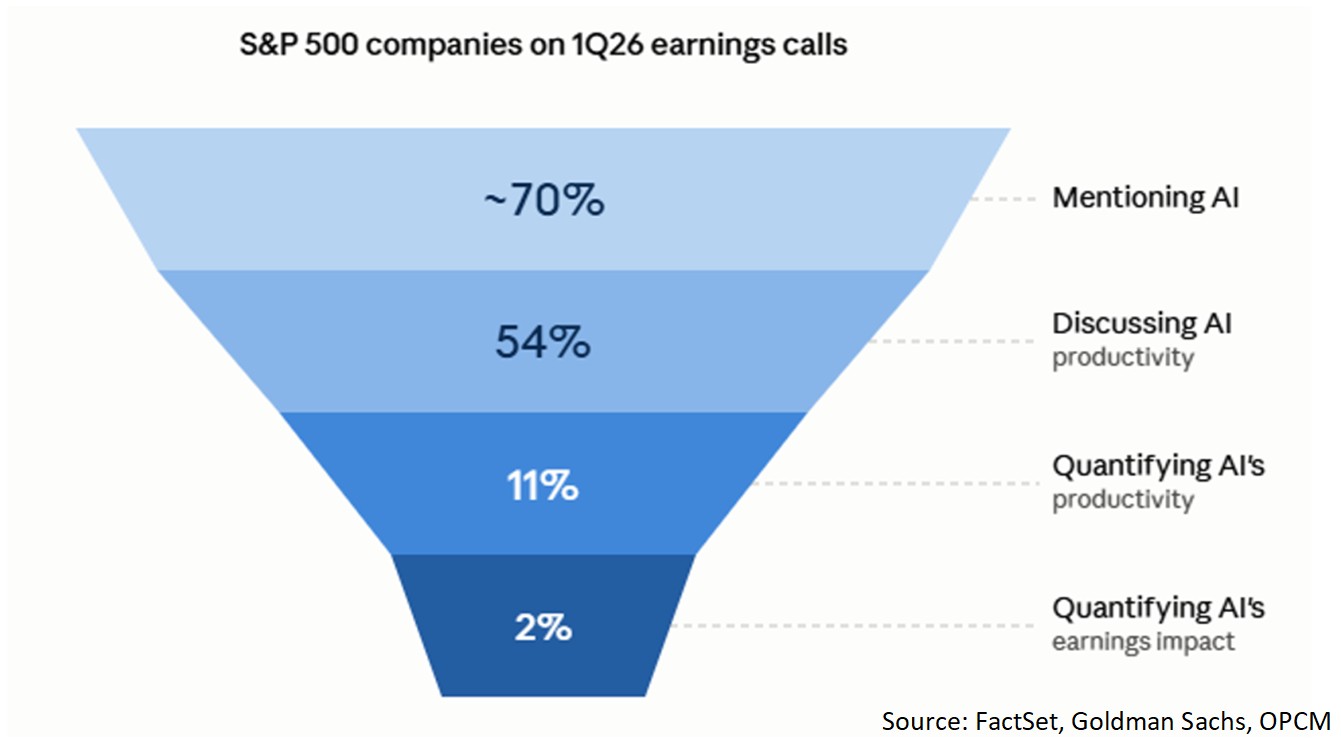

Improving capabilities combined with declining costs have helped accelerate adoption. Consumer adoption of generative AI exploded first. OpenAI’s ChatGPT has over 1 billion monthly active app users. Google’s Gemini has over 900 million. Enterprise AI adoption is also high as some surveys suggest around 90% or more of enterprises use AI in at least one business function, mostly in the form of generative tools. Meanwhile, enterprises are definitely talking about AI. During the first quarter of 2026, almost 70% of S&P 500 companies mentioned AI on their conference calls, which compares to 25% three years ago and 45% last year.

Productivity gains will act as a key driver of future agentic AI enterprise adoption. Currently there is a big spread between the percentage of S&P 500 companies mentioning AI on conference calls and those able to quantify AI’s productivity impact let alone its earnings impact.

Companies are wrestling with numerous issues trying to structure an AI strategy that leverages agentic AI for earnings improvement. Fragmented data and antiquated tools often are not ready for agentic AI workflows. Enterprise security requirements must be met, and given how quickly AI models are advancing, some enterprise administrators are reticent to provide AI models access to enterprise resources. Enterprises are increasingly questioning the data governance of AI models; they do not want model developers like Anthropic and OpenAI to end up using the enterprise data to train OpenAI and Anthropic internal offerings to compete with those same enterprises. Finally, agentic AI requires redesigning workflow processes.

Without having a structured AI strategy, agentic AI costs can quickly blow through budgets, as evidenced by some major enterprises in the first half of 2026. This is because, even though AI token costs are declining, agentic AI can be 1000x more token intensive than a standard chatbot query.

If these issues are solved, the gap between the number of companies talking about AI and those able to quantify its productivity impact on earnings should shrink.

Volatility

A question, however, is how quickly it will shrink. Amid record returns, investors accelerate expected timelines for positive outcomes and assume there is only upside volatility.

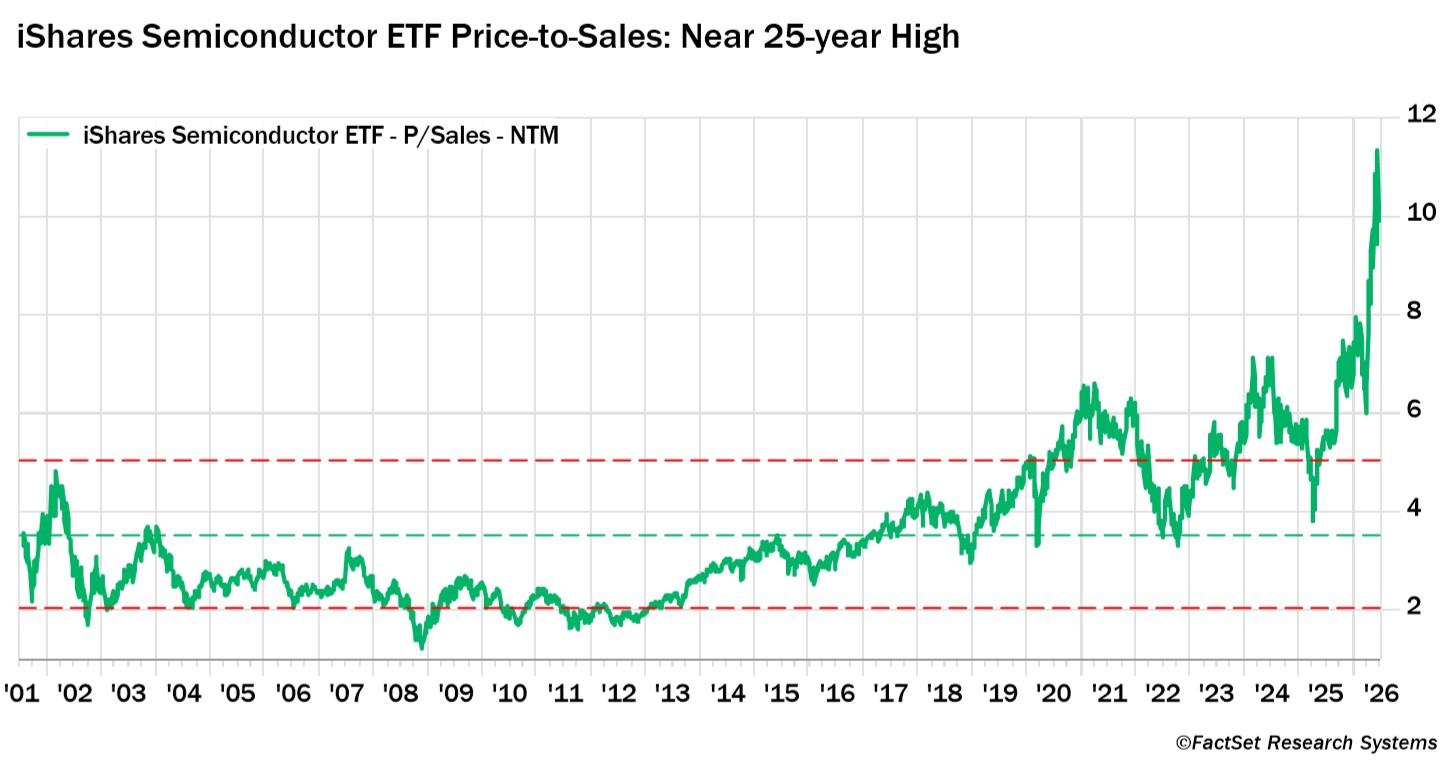

One could argue that is where some hot areas of the market like semiconductors sit today. The semiconductor industry now trades at almost 11 times forward revenue, similar to levels seen in March 2000.

This can set investors up for periods of disappointment. Consider the last major technology investment cycle. The cycle bore tremendous fruit for the economy. But the volatile path created many buying and selling opportunities. From 1995 – 1998, semiconductors saw two 50% drawdowns on their way to record highs hit in 2000 before yet another major drawdown. Small hiccups in demand, supply shortages getting addressed, and external macro or policy shocks that impact risk appetite can drive downside volatility.

The Osborne Partners Investment Team strives to manage risk prudently, reducing exposure when the risk-adjusted upside no longer justifies it, and increasing exposure when it does. We will continue to do so as the AI cycle evolves.