Over the past few years, multi-asset class investing has not been kind to many large and well-known foundations and endowments. Many of these previously solid managers have delivered the combination of poor returns, coupled with high fees, and abnormally high volatility. Sentiment has become increasingly negative for a management style that delivered the best risk-adjusted returns for many decades. Media stories have ramped as coverage of Harvard’s layoff of half of their investment staff found its way onto front pages of numerous publications earlier this year. As seen below, only one Ivy League school delivered a positive 2016 fiscal year return.

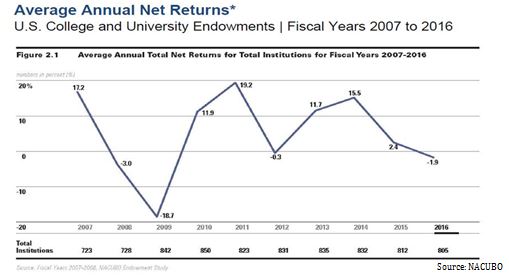

The average U.S. college and university endowment did not fare any better, with the average posting a negative 2% return in fiscal year 2016, as seen in the following chart.

How did arguably the world’s most successful risk-adjusted management style perform so poorly recently? We believe it was caused by a combination of management missteps and once-in-a-century market conditions for many asset classes.

First, regarding the management missteps, many endowments and foundations entered the 2007 bear market with generally high equity allocations. The table below shows the average allocation for institutional investors. At the top of the market for equities in 2007, the average institution had a similar allocation to the 2005 bar – approximately 55% allocated to global equities. Through the bear market, institutions actually reduced holdings of equities, and by the time stocks bottomed in 2009/2010, equities allocations were down to under 45%. As you can see, through 2013, and still evident today, these managers have further reduced equities to under 35% in 2013.

Many high-profile endowments have spent the last few years with total equities allocations under 30%. Over the past 5+ years, most of these managers increased their allocations to other asset classes, most notably alternative asset classes – defined as hedge funds or other hedging tools, private investments, and natural resources. These investments dramatically underperformed equities recently. So from an allocation standpoint, these endowments shifted out of equities fearing another bear market, just as the equities asset class, especially in the U.S. posted excellent returns.

On the management side, the allocation missteps were further compounded with high expenses. Most foundation and endowment managers not only use outside firms to manage their assets, which require paying another layer of fees, but the endowment managers additionally employed a deep staff of professionals to “manage the managers”. These foundations learned it is a poor combination when returns are difficult to generate, you pay multiple layers of management fees and many of the investments are illiquid.

Next, certain market variables have been working against this style for the past 5+ years, most notably a strong dollar and historically low interest rates. The dollar headwinds for multi-asset class date back to the 2008-2009 recession when global central banks lowered interest rates to essentially zero. As the U.S. exited the recession before most other countries, the U.S. dollar bottomed in 2011 versus other currencies. After a trading range, the dollar exploded, climbing nearly 30% from 2014-2016 as the U.S economy improved (chart below), while parts of the globe continued to labor through the issues from 2008-2009. The strength of the U.S. dollar was a headwind for two important asset classes, foreign equities and natural resources.

The historic low interest rates affected multi-asset class investing a different way, mainly by propping up Real Estate Investment Trust (REIT) valuations due to their higher dividend yield characteristics, along with allowing U.S. equities valuation multiples to rise with bonds as a competing asset class providing poor income with low interest rates. The chart below depicts the action in interest rates from the previous stock market top through today for the ten-year U.S. Treasury. Interest rates fell from 5.35% to only 1.35%.

Due to this partially manipulated drop in interest rates, Real Estate Investment Trusts (REIT) are now exceedingly valued with very high valuation multiples and very low cap rates. Meanwhile U.S. equities are now trading at close to 19 times forward earnings versus a long-term average of just over 15 times. “Bond proxies” within U.S. equities are even more expensive, especially considering their low earnings growth profile. Examples are utilities, consumer staples, and telecom services companies.

While all of these factors have led to difficult returns for multi-asset class investing, there are reasons to believe this underperformance is poised to reverse. First, the dollar has fallen 7% as our Federal Reserve begins to increase short-term interest rates, just as economies outside the U.S. are improving. The dollar’s fall is partially due to the belief that once a central bank lifts rates, the economy eventually slows. Additionally, economies outside the U.S. started to rebound. As the U.S. dollar’s strength subsides, foreign equities have started to outperform the U.S. The dollar weakness should eventually be a tailwind for the underperforming natural resources asset class.

Further, as U.S. interest rates bottom, the mispricings in real estate and certain U.S. equity sectors should reverse. U.S. REITs may continue to underperform as they have recently, while low growth/high yielding sectors like utilities, telecommunications service, and consumer staples may rerate to lower valuations.

Next, valuations for asset classes such as foreign equities and natural resources may become too tempting for investors to avoid, as the risk/reward has become extremely positive. Prior to 2017’s outperformance, foreign equities were essentially left for dead as the valuation discount versus U.S. equities grew to decade long extremes.

Finally, when you examine the recent asset class returns versus their long-term averages, one should be very comfortable owning a blend of multiple asset classes, with the possible exception of U.S. equities. They are not only mildly overvalued to us, but are the only asset class to deliver a higher return from 2011-2016 than the 40-year average. The table below, shows the 2011-2016 annualized return of each asset class versus its 40-year average. While U.S. equities have outperformed their long-term average, asset classes like foreign equities, natural resources, and alternative assets like hedge funds, have underperformed their long-term averages by as much as 16% per year from 2011-2016. More importantly, a simple equal weighted multi-asset class portfolio has only generated a 2.6% annual return – hence the negative sentiment about foundation and endowment management. Over 40 years, an investor earned about 8.6% per year with an equally weighted portfolio, and more importantly enjoyed lower volatility and fewer down years than single asset classes.

OPCM is a multi-asset class manager, yet our returns have outpaced the foundation and endowment management crowd during this difficult period. How did this happen? We believe the answer is both qualitative and quantitative. First, on the qualitative side, we manage portfolios in-house using individual securities. This means clients do not pay fees to other managers along with us to manage the managers. Plus, we always know exactly what we own versus attempting to track what multiple managers are doing day to day. This also aids in our tax-efficient management. Second, we keep transaction costs low. Third, we use liquid investments. On the quantitative side, we actively manage portfolios, and make subtle shifts between asset classes versus owning static investments. We use deep fundamental, valuation, and sentiment analysis for each individual investment decision, along with each asset class adjustment.

The potential for multi-asset class investing to return to its long-term risk and return advantages excites us, especially considering our returns have been positive through this difficult period for the style. Many of the subtle shifts we made over the last year such as increasing foreign equities, building our natural resource allocation after years of being underinvested, and reducing our real estate holdings are beginning to propel the overall portfolio. As the recently poor performing asset classes start to reverse, our diverse portfolio should continue to perform well as U.S. equities begin to underperform at some point in the future. Many investors who are now dramatically overweight U.S. equities, and have shifted away from recently underperforming asset classes will see the downside of single asset class investing and performance chasing.