Growth investors are increasingly willing to pay practically any price for companies with strong earnings growth in this slow growth environment. Conversely, income investors are increasingly willing to overpay for companies that pay higher dividends and a higher yield than the presently low yields on bonds. These two abnormal and high risk strategies have caused domestic equities markets to be led by a very narrow subset consisting of utilities, consumer staples, telecommunications service, and internet/social media stocks.

In 2015, equity markets were flat overall. The S&P 500 was down for the year until a rally during the final week of the year pushed it into positive territory. Meanwhile small-cap stocks fell over 5% as exorbitant valuations finally caught up with the Russell 2000®. However, the S&P Internet Software and Services Index was up 34% as investors were willing to “pay anything for growth”.

During the first four months of 2016, both the S&P 500 and small-cap stocks were essentially unchanged for the year. However, utilities and telecommunications services companies were up over 10% for the year, while consumer staples were strong performers as well. Why? Income investors have become dangerously comfortable overpaying to receive the bond-like dividend yields these sectors provide.

It is easy to see why growth investors and income investors are willing to pay major valuation premiums. At this moment, valuations don’t matter. However, there will be a point, possibly soon, when valuations do matter. This time will be painful for these investors. To show how investors are overpaying, we provided two tables.

The first table shows historic and present price/earnings and earnings growth metrics. For example, over the last 20 years, utilities stocks have traded at an average P/E on forward earnings of 14.8x. At the start of the fourth quarter of 2013, utilities traded at a fair P/E of 15x. With the major outperformance over the past few years, the forward P/E of utilities has risen to 18x, which is a 20% increase since late 2013 and 22% above the long-term average. This indicates utilities are quite expensive versus history. Meanwhile earnings growth has only risen 4% per year over the last few years, meaning earnings have only grown half as fast as the P/E growth. Looking at consumer staples, the metrics are even more staggering as P/E’s are up 33% while earnings will have barely grown by 3% per year by the time 2016 ends.

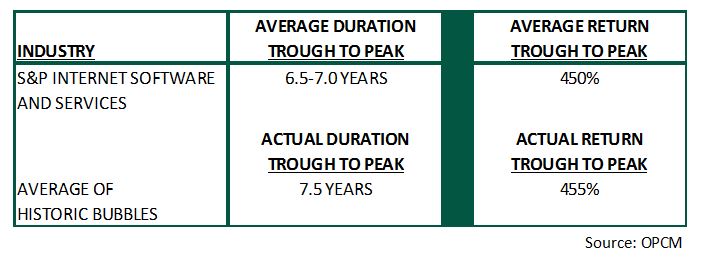

The second table refers to the rapid price appreciation in internet stocks. Remember, these are stocks that trade at extremely high valuations, but their earnings growth is supposed to offset the seemingly irrational valuations. This industry comprised of high fliers like Facebook, LinkedIn, Verisign, and Salesforce, trade at an enterprise value (EV) to EBITDA premium of three times the S&P 500. The table simply compares the prolific 455% rise in internet stocks over the last 7.5 years to the average duration and return of a group of the most well-known bubbles in history – the 1920’s stock market bubble, the 1970’s oil bubble, the 1980’s Japanese stock market bubble, the 1990’s internet bubble, and the 2000’s housing bubble. The result is growth investors have continued to overpay for internet stocks to the point where the price appreciation has matched, both in duration and return, many of the most significant bubbles in history.

The unfortunate phase of a bubble phenomenon occurs once it peaks. The average fall is approximately 65%, and the bubble unwinds two or three times faster than it rose.

Our main point is: due to our methodical discipline, we are avoiding investments in these dangerously valued areas of equities. Careless focus on short-term, momentum-driven returns can jeopardize long-term wealth. Shorter-term this positioning can be frustrating as slow-growing, high debt sectors like utilities continue to march higher, while some internet stocks pop 10% in a day due to a positively perceived earnings release. Time-tested disciplines matter, and investors will once again learn valuations inevitably matter.