In recent weeks as financial markets reeled in response to ongoing coronavirus headlines, few asset classes were spared. Even parts of investment grade Fixed Income, the asset class intended to act as a buffer to more risky asset classes, saw stress. Aside from cash and some areas of Fixed Income, there weren’t many places investors could hide. Real Estate, an asset class that can be particularly sensitive to changes in economic activity, fared worse than most. From February 21th until March 23rd, U.S. REITs were down approximately 44%. This decline marked the third worst sell off in history with the other two occurring in the midst of the 2008-2009 financial crisis. In the wake of the recent decline, we are now seeing more attractive opportunities in Real Estate than any point in the past decade. In this article, we will take a look at how our team has managed Real Estate in recent years; explore what the post-coronavirus landscape may look like for the asset class and take a closer look at the opportunities that have emerged.

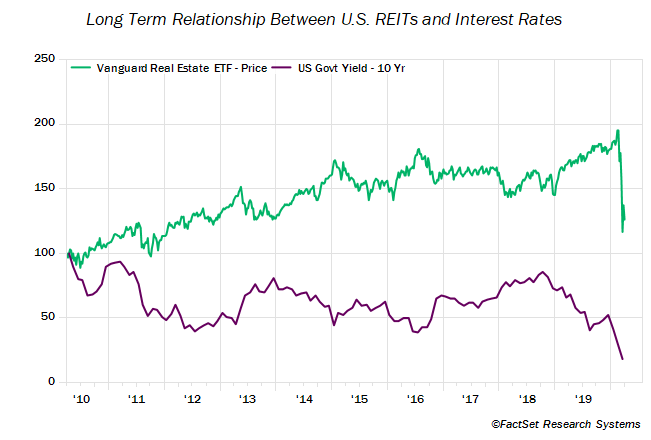

Investments within the Real Estate asset class typically fall into one of two broad buckets: U.S. & International REITs (real estate investment trusts, entities that own physical real estate and carry tax advantaged status) or traditional corporations involved in one or more areas of real estate (homebuilders, real estate brokers, etc). Both types of assets are sensitive to interest rates and the general level of economic activity. When interest rates are low, consumers and companies benefit from cheaper mortgage rates (benefiting homebuilders and real estate brokers), and REITs typically draw more interest from investors attracted to the relatively higher yields that most offer. Over the past decade, a period marked by low interest rates across the globe, REITs have been amongst the best performing asset classes, second only to large cap U.S. equities. While pleased with the stellar performance, it has made for a very challenging environment to find new investments that trade at attractive valuations. As such, up until just recently, changes to the asset class more often involved sales than buys.

Much of the recent debate surrounding COVID-19 and the economy has been how soon can we re-open? There is speculation it could be as early as a few weeks while other say it could be months, but regardless of when it happens, there will be fundamental differences in the pre and post COVID-19 economy. Unfortunately, unemployment is expected to be markedly higher and chances are that we will see a more cautious consumer, at least initially. This will weigh on real estate sectors like lodging, gaming and malls. Companies operating with fewer employees or employees more inclined to work from home could dampen demand for office space, which could weigh on REITs which own office buildings. But all of the changes won’t be negative –some sectors could emerge relatively unscathed or on even better footing than before. One of the early trends resulting from the pandemic has been a surge in internet traffic as individuals cooped up at home increase their social media activity, online shopping and video chats. This is likely to benefit REITs that own data center infrastructure. REITs that own real estate involved with healthcare services, storage, and other essential service buildings may also fare better than most. Given the varied impact COVID-19 will have on various sectors, being selective and paying attention to valuations will be imperative.

As mentioned above, U.S. REITs fell over 40% over the course of roughly one month. Any time such a dramatic selloff occurs in such a short period of time, there always exists a fair amount of capitulation, panic and ultimately, investment opportunities that come about very, very rarely. So far the opportunities that we are seeing exist in one of two forms: companies that are likely to be directly impacted by COVID-19 but markets have been overly punitive to the stock, OR companies that are unlikely to see much of an impact but have still sold off a meaningful amount. We are seeing opportunities across many sectors and industries as markets still try to sort out which industries will be impacted and to what extent. Another reason we find the opportunities within Real Estate particularly attractive now is due to what has happened to interest rates. After starting the year slightly under 2%, the 10-Year U.S. Treasury yield dipped below 0.5% in mid-March, marking an all-time low. The implications for the Real Estate asset class could be meaningful. With interest rates low, consumers will look to take advantage by taking out cheap mortgages, potentially helping the residential real estate market. Additionally, REITs are highly dependent on issuing debt and equity to fund their growth. As equity markets recover and assuming interest rates stay low, REITs will have a cheap source of capital to buy or build new properties, all while continuing to offer attractive yields.

On several occasions in recent years, the investment team has been asked why we don’t have higher allocations to our Real Estate asset class. After all, it had been one of the better performing asset classes. One common response was that valuations had crept up to levels that were far too demanding given the stable but relatively unimpressive underlying fundamentals. In order for our team to allocate cash towards a new investment in Real Estate or any asset class, it needs to offer a compelling risk/reward. While it has been challenging to find such opportunities in recent years, conditions have changed quickly and we have become more enthusiastic about the opportunity set in front of us. Our fantastic team of Portfolio Counselors, as well as the Investment Team, look forward to sharing more with you soon.