The U.S. housing market has been stuck in neutral for quite some time. After a short burst of enthusiasm in the years following the pandemic, momentum has slowed considerably. While several factors have played a role, the primary culprit has been interest rates, which have been high and slow to retreat. And with economic growth remaining muted, there’s been little help from other corners. Buyers face an unfortunate reality: rates are high, and prices are too. So, what gives first? In this article, we’ll take a high-level look at the U.S. housing market, explore the forces most likely to influence its trajectory in the years ahead, and discuss how we approach investing in the space during this period.

2020–2021: The Pandemic-Induced Boom

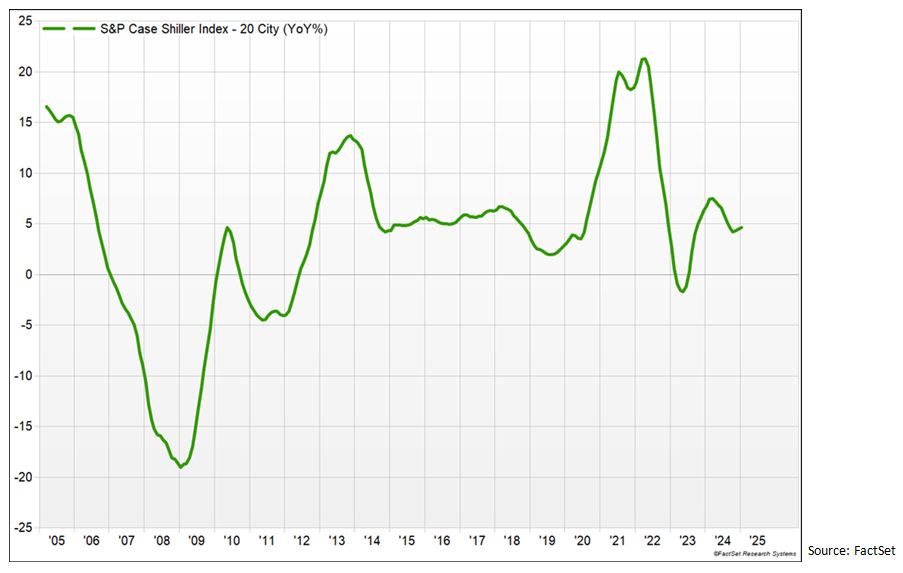

When COVID-19 struck in early 2020, no one could predict the shape of the weeks and months that followed. As the global economy ground to a halt, one of the immediate economic side effects was a collapse in interest rates. The Federal Reserve and central banks around the world slashed borrowing costs to near-zero, aiming to stabilize the global economy. In the U.S., this translated into historically low mortgage rates – sparking a wave of buying and refinancing as millions of homeowners locked in mortgages with sub-4% rates.

By the end of 2021, an estimated 60% of U.S. homeowners had mortgages under 4%, a dramatic shift from just 10% a decade earlier. Meanwhile, the share of 30-year mortgages with rates over 6% had bottomed out at a mere 3.7%. The combination of ultra-low borrowing costs, pent-up demand, and massive fiscal and monetary stimulus unleashed a mini-boom in the housing market.

But that boom came with consequences. The sudden and dramatic surge in demand collided with pandemic-driven supply constraints, sending home prices surging. The housing market’s strength contributed to a broader rise in inflation – one not seen in the U.S. since the early 1980s, with annual inflation eventually topping 7.5%.

2022–Today: The Hangover

The Federal Reserve, which for a period was seemingly tolerant of rising inflation, reversed course quickly. In March 2022, it initiated the first in a rapid series of rate hikes, totaling over 500 basis points (5%) within just 16 months. Mortgage rates followed suit. After starting 2022 at just over 3%, the average 30-year fixed mortgage rate soared past 7% by year’s end.

For a housing market accustomed to borrowing costs between 2.5% and 5%, this was a seismic shift. With most homeowners holding mortgages well below prevailing rates, housing related activity slowed dramatically. Homeowners simply weren’t willing to trade a 3% mortgage for one north of 6.5%, with many opting to stay put.

This is evident by looking at existing home sales in the U.S. which collapsed – from 6.1 million in 2021 to just 4.07 million in 2024. To put that in context, that’s below levels seen at the depths of the 2008 financial crisis, when sales troughed at 4.1 million. New home sales also took a hit, falling roughly 30% between the end of 2021 and 2024.

Yet, despite this deep freeze in activity, prices didn’t fall. In fact, they’ve continued rising modestly – defying predictions of a housing crash. For now, the specter of a 2008-style collapse remains elusive and unlikely.

What Gives?

With both interest rates and home prices hovering near multi-decade highs, something has to give. We believe interest rates are the more likely variable to adjust. There are several reasons. First, it is in the best interest of the Federal Reserve – and broader U.S. economic policymakers – to gradually bring rates down without triggering a dramatic correction in home prices. Stability in housing is crucial to the broader economy. Second, while inflation has proven more persistent than expected, we believe the long-term trend still points lower. As it softens, so too should interest rates.

History is supportive of this idea. Over the past 30+ years, material declines in U.S. home prices have been rare. Outside of the 2007-2009 financial crisis, material declines in home prices within the U.S. have been incredibly rare, even during recessions. When prices have fallen, the declines have typically been modest and short-lived.

Investing Through the Cycle

From a portfolio management perspective, the current market presents unique opportunities. For the first time in several years, our Investment Team is beginning to warm up to U.S. homebuilders as potential investments. As of this writing, many U.S.-listed homebuilders have declined over 30% from their October 2024 highs. If mortgage rates decline meaningfully, homebuilders stand to benefit significantly.

We’re also keeping a close eye on adjacent sectors like manufactured housing REITs, which offer more affordable housing alternatives for Americans who have been priced out of traditional home ownership or simply find more value in cost-effective manufactured homes.

The U.S. housing market remains in a holding pattern, with buyers and sellers both parked on the sidelines. Yet while housing activity has largely stalled, opportunities for investing in the housing market have not. We believe a path to normalization – likely led by lower rates – will gradually restore health to the housing sector. In the meantime, our focus remains on finding high-quality investment opportunities within the industry that complement our broader portfolios, since this period of housing inactivity won’t last forever.