There is no denying that electric vehicles (EV) are on the precipice of changing the world of mobility. The disruption brought by this change will likely crown new industry leaders while toppling legacy incumbents that fail to adapt. However, the market enthusiasm for all things electric, including battery and EV manufacturers is bordering on mania. While an electric future is exciting, the current valuations of the majority of EV companies and historical precedent from other periods of innovation indicate that they represent poor investment opportunities today. To understand why, it’s important to understand how we analyze individual stocks, including the potential risks and rewards of an investment.

At Osborne Partners, we take great pride in our rigorous investment research process. Before we consider a stock purchase, we spend significant time understanding a company’s operations, growth and profit opportunities, industry and competitors, and valuation. At the end of our research process, we distill our analysis into two price targets representing potential upside and downside scenarios. The upside target represents the price that we believe the stock would likely trade at if our investment thesis plays out as expected. The downside target represents the price we believe the stock could trade at in a more adverse situation where our thesis doesn’t play out as expected. The ratio of the gain from a stock reaching our upside price divided by the loss of it falling to our downside price comprises our risk-reward metric. We prefer this ratio to be greater than 2:1, meaning the potential gains from an investment are double the downside risk of loss.

While each company’s analysis is different, in general, we establish an upside price target by setting realistic expectations for future fundamentals and applying a reasonable valuation multiple. What do we mean by reasonable? We consider the company’s and industry’s historical growth rates, any fundamental changes that could cause a positive inflection in growth, and the interplay between the current economic cycle and business or industry fundamentals. For valuation, we use a wide variety of valuation metrics to establish our price targets. In setting our target multiple, we review the company’s historical valuation range, the valuation of its peers, and valuation changes throughout the economic cycle. Establishing a downside price considers the same variables but in reverse, including how far earnings and valuation multiples have fallen in previous recessions or periods of challenged fundamentals. We are intentionally conservative in setting these targets since a mistake, especially in the downside target, could lead to substantial losses.

We also identify the key catalysts for a company in the coming 12-18 months that will likely move the stock price towards our upside or downside targets. These catalysts often include earnings announcements, new product launches, potential acquisitions or divestitures, and economic developments. We regularly monitor and update our price targets and catalysts for our holdings to ensure that our portfolio’s risk-reward ratio skews positive. A narrowing risk-reward ratio will often lead us to sell or trim a position.

Using this risk-reward framework, we can interpret what the market is “pricing in” for individual companies. Suppose the market is “pricing in” only a bullish scenario. In that case, the risk-reward will be negative (downside risk greater than upside potential), and the stock price will likely decline if the company fails to achieve the bullish outcome expected. Conversely, the market may be “pricing in” a bearish scenario. In that case, the risk-reward will be positive (upside potential greater than downside risk), and the stock price will likely gain if the company performs even modestly better than expected. Companies are usually somewhere between these two extremes, and making declarations that the market is clearly “pricing in” one extreme or the other is difficult. However, within the EV ecosystem, the market is clearly “pricing in” only the most bullish outcomes for numerous companies.

The electric vehicle industry, including battery and electric vehicle manufacturers, is generally in a state of speculative mania reminiscent of the dotcom boom. According to data compiled by BloombergNEF, a provider of financial data, EV companies raised nearly $25 billion via initial public offerings (IPO), secondary share sales, and special purpose acquisition company (SPAC) mergers in 2020, up from just $1.6 billion in 2019.[1] The explosion of capital chasing EV investments has been spectacular, and the valuations attached to these companies are equally extraordinary.

The battery market has seen company valuations increase substantially over the past year. The battery market is relatively concentrated, with Chinese CATL and Japanese Panasonic accounting for more than 50% of total production, with the balance coming primarily from other Asian manufactures, including LG Chem, BYD, and Samsung SDI. These companies are not readily available for purchase on U.S. exchanges, though we would not be looking to purchase them today even if they were. Battery companies currently trade at very high valuations, reflecting expectations for accelerating battery demand and a lack of new entrants into the market. As measured by their average forward P/E, the valuation of these five companies has increased by 120% to 65x forward earnings since the end of 2019. CATL and BYD, the companies with the most battery exposure, have forward P/E ratios exceeding 100x. These valuations are likely unsustainable.

Battery startups have even higher valuations. QuantumScape (QS), a U.S.-based manufacturer of solid-state batteries that went public via a SPAC merger late last year, has a market capitalization of more than $18 billion today, though down from over $40 billion at the end of 2020. This valuation is despite a lack of revenue today and no meaningful revenue expected for the next several years. According to QuantumScape’s own financial projections, annual revenue will only exceed $100 million in 2026. The valuation of QS is completely divorced from any business fundamentals. While solid-state batteries are expected to represent the next revolution in battery technology, the technology is still being developed and has yet to be successfully commercialized. Investors in QS will likely experience disappointing returns if the technology’s commercialization never occurs, commercialization takes longer than expected, or another company ends up leading the market. Even if everything goes right for QS, the returns to shareholders may still be disappointing.

The market valuations of electric vehicle manufacturers make the valuations of battery manufacturers look almost pedestrian. Currently Tesla trades at a forward price to earnings ratio of 180x, up from 66x at the end of 2019, and has a market capitalization of over $750 billion, making it worth about the same amount as the ten largest auto manufacturers combined. For comparison, the ten largest auto manufacturers (VW, Toyota, GM, etc.) have annual sales of over $1.5 trillion and manufacture more than 50 million vehicles annually. Tesla had sales of $32 billion, profits of $2.5 billion, and manufactured 500,000 vehicles in 2020. It appears that the market is “pricing in” a future where Tesla is the only automobile manufacturer left. As with battery manufacturers, we see significant downside risk for Tesla’s stock price. One thing to keep in mind is that a good company doesn’t always equate to a good investment. Tesla is a great company that is changing the world for the better but represents a risky investment opportunity at today’s price and valuation.

Electric vehicle startups with little to no sales appear to be even more highly valued. Starting a car company is a risky undertaking. Despite being successful today, if overvalued, Tesla nearly went bankrupt multiple times as manufacturing and product development setbacks nearly sank the company. However, the market is assigning multi-billion-dollar valuations to EV manufacturers that have yet to deliver a single vehicle. Churchill Capital Corp IV (CCIV) is a SPAC that is rumored to be in talks to merge with Lucid Motors, a luxury EV startup, and is up nearly 500% at the time of this writing on just the rumors alone. There have been recent market rumors about Rivian, an EV truck manufacturer, going public later this year via an IPO with a $50 billion valuation. While Rivian has the backing of Amazon and Ford, it has yet to deliver a single vehicle to customers. Startups may not have the easy path to success that these valuations imply. Legacy auto manufacturers are investing tens of billions of dollars each to ensure they can compete with Tesla and the various startups. Becoming the next VW or GM will not be easy, and many of these new entrants will likely fail long before they have a shot. The valuations for EV companies points to market excess and speculation boarding on mania; we have seen this story before, and we know where it will likely end.

Using our risk-reward framework, neither battery manufacturers nor electric vehicle companies are investable given that their downside risk exceeds the maximum downside we typically tolerate when purchasing a stock – generally about 20% to 30%. When a stock has such significant downside risk, we would need to reasonably believe that its prices could more than double based on company fundamentals even to begin to contemplate adding it to our portfolio. However, even if we did believe a stock could experience large enough price gains to give the stock a risk-reward ratio of 2:1, the risk of substantial losses would generally prevent us from purchasing it.

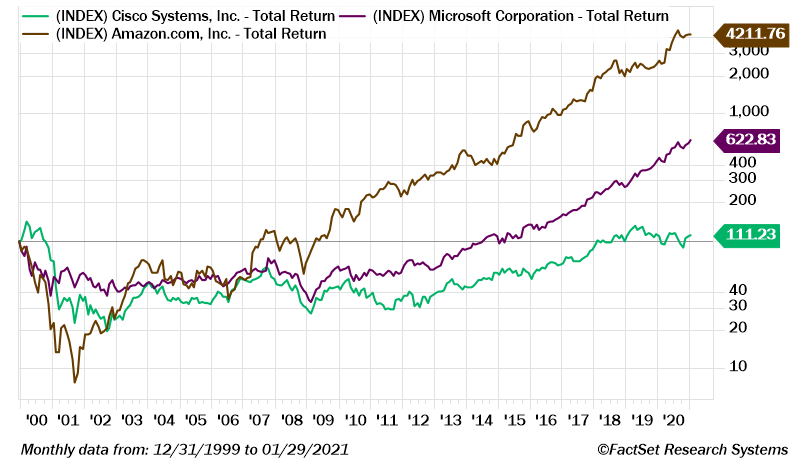

Assuming these companies don’t fail, the key risk is that their stock prices are so overvalued today that it may take a decade or more for their stock prices to recover after the current euphoria eventually passes. Looking at three dotcom bubble survivors (Cisco, Microsoft, and Amazon) is instructive. As the chart below demonstrates, despite surviving the dotcom carnage, Amazon took seven years for its stock price to recover to the end of 1999 price, Microsoft took nearly 14 years, and Cisco took almost two decades. At the end of 1999, the market was “pricing in” only the most bullish scenarios for these companies. Once the market adopted less bullish outlooks for these companies, it took nearly a decade or longer for investors to recover their losses.

We are not against investing in the electric revolution, and in fact, we have unique EV exposure in our portfolio already. We own a leading manufacturer of automotive semiconductors that benefits from increased chip content in EVs relative to internal combustion cars. The holding trades at a forward P/E of less than 20x. We also hold a leading auto parts manufacturer that is a leading supplier of EV drivetrains, and also partially owns a battery pack supplier that recently went public via a SPAC merger. Additionally, this holding recently announced that it is acquiring a commercial vehicle battery pack manufacturer, further expanding its EV capabilities and offerings. The stock trades at a forward P/E of just 11x. Finally, since March 2020, we have owned the highest quality copper miner. EVs require four times as much copper content as combustion engines.

While the appeal of investing in the next great innovation is undeniable, the fact is that for most investors, the stock performance rarely matches the hype. We use the risk-reward framework discussed here to help ensure that the investments we make are prudent and appropriate, with the risk of potential losses more than offset by the reward of potentially greater gains. By focusing on not just what can go right with an investment but what can also go wrong, we seek to avoid investments where the downside risk exceeds any reasonable expectation of what the potential gains could be. While it is difficult to watch the stock of a company you admire, but don’t own, continue higher month after month, you will eventually be thankful that you stuck with a disciplined investment strategy and sat on the sidelines.

[1] https://assets.bbhub.io/professional/sites/24/Energy-Transition-Investment-Trends_Free-Summary_Jan2021.pdf