We are three quarters of the way through 2016 and one of the more interesting stories of the year thus far has been the resurgence of gold. The polarizing metal is up over 20% through September and seems to have worked its way back into investors’ good graces after several years of disappointing returns. In fact, there was more investor demand for gold in the first two quarters of 2016 than we saw in all of 2014 or 2015. So what has caused this sudden about face? There hasn’t been one specific catalyst, instead a combination of things have contributed to this change in investor sentiment including: Brexit, the U.S. Presidential Election, negative interest rates, concerns around global debt levels and general sluggish economic strength. With the increased attention gold is getting this year we have received several questions about what role gold should play in a diversified portfolio (if any). In this article we will explore this question and take a look at the merits of owning the yellow metal.

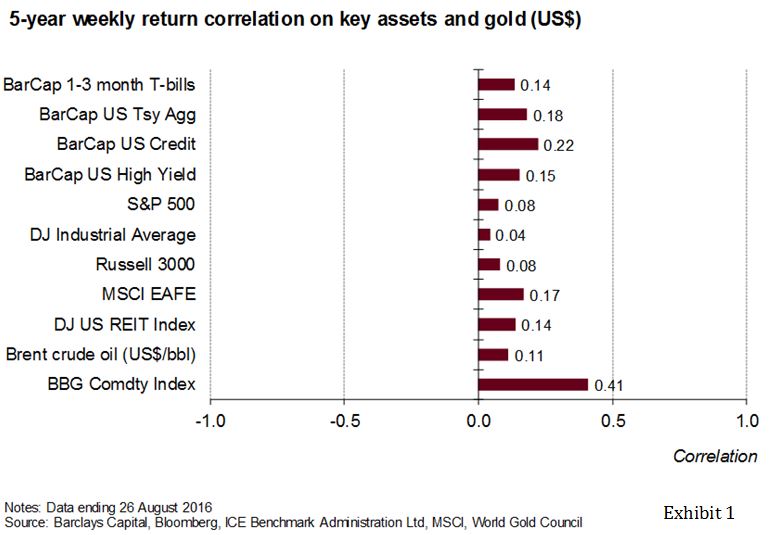

Ask three investment professionals their opinion on owning gold as a stand-alone investment and you’re likely to hear three completely different answers. Despite this, one thing that is commonly agreed upon is the diversification benefits that gold (and other precious metals) can bring to a portfolio. The foundation of portfolio diversification is built on the premise that owning a basket of non-correlated assets will reduce the overall risk of the portfolio. Decades ago, investors typically thought buying a few bonds would diversify a portfolio of stocks. Today, assets like foreign equities, natural resources and real estate have gained acceptance in a diversified portfolio, and have shown to effectively reduce the overall volatility in a portfolio. This is where the benefit of owning gold in a portfolio can really be seen. Gold has some of the lowest correlations to other conventional asset classes as seen below.

Even more significant, the correlation between gold and equities has typically fallen during periods of market stress. In other words, when equity markets start performing poorly, gold has typically performed well (see Exhibit 2). There are several reasons that help to explain this phenomenon with the most logical being that when investors lose faith in stocks (and/or other asset classes) they typically view gold as a relative safe-haven. This can be seen in the strong negative relationship that has existed between gold prices and consumer confidence over the past 50 years.

Another common role that gold plays in a diversified portfolio is to hedge against inflation. And, since inflation often coincides with a falling U.S. dollar it also serves as a currency hedge (see Exhibit 3). Given that inflation has been relatively benign and the dollar has been uncharacteristically strong in recent years, neither of these risks have been a chief concern for investors – until recently that is. In June of 2014, in an attempt to jumpstart economic growth and inflation, the European Central Bank introduced negative interest rates and became the first major central bank to do so. At the time it raised a few eyebrows but was widely viewed as a short-term experiment intended to boost growth. Then, in January of this year, the Bank of Japan followed suit and also introduced negative interest rates. Since this decision by the BoJ, skepticism has grown around the efficacy of current monetary policies and the potential ramifications they may have, particularly on inflation and global currencies. In fact, we are starting to hear more investors proclaim that investing in gold is an outright hedge against misguided central bank policies. Whether or not these unique monetary policies result in the failure that some are suggesting remains to be seen and any declarations that these policies have been a failure are likely a bit premature. Regardless, we agree that it is prudent to own gold in the current environment and have held this belief for the past few years.

As an investment team, we take a bottom-up approach to analyzing investments. For example, when analyzing an individual company, this means scrutinizing a company’s income statement, balance sheet, cash flow statement, valuations metrics and industry outlook, amongst many other considerations. Because gold is a commodity, it doesn’t produce ongoing cash flow or pay a dividend yield, which is part of the reason that analyzing it as an investment can be perplexing or even challenging at times. It was in this vein that Warren Buffet once said, “Gold, however, has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end.” Despite its shortcomings we maintain that gold’s role in a portfolio is validated by its superior diversification qualities as well as its ability to help hedge against inflation risk, currency fluctuations and maybe even precarious monetary policy.