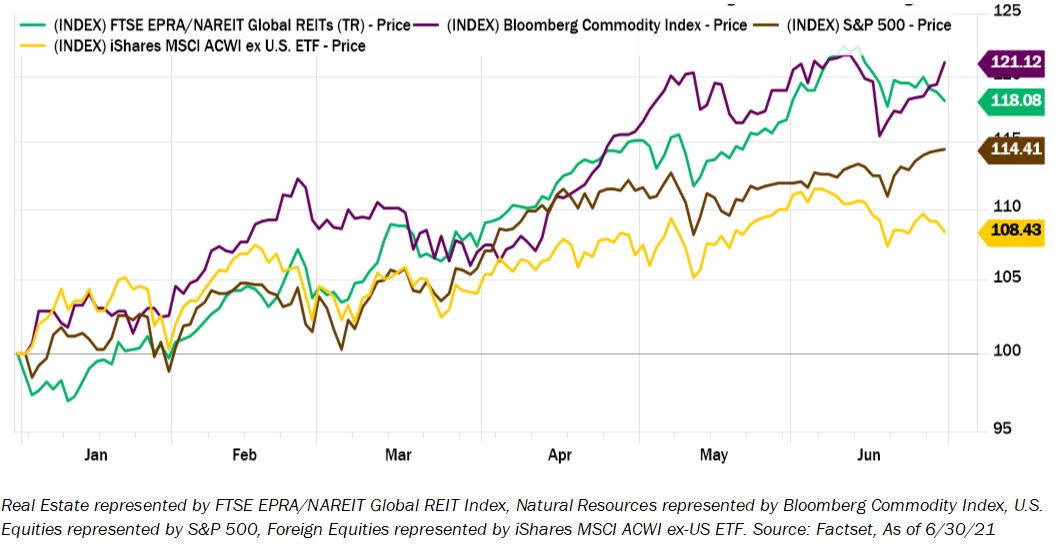

Through the first half of 2021, Natural Resources and Real Estate are amongst the best performing asset classes – we’ll look at what drove this performance and offer an outlook for the second half.

Thinking back to 2020 and everything that transpired in financial markets, amongst the most incredible developments was not only the speed and magnitude of the bear market that swept across the world but also the pace at which financial markets recovered. U.S. and Foreign Equities, both of which fell roughly 35%, were back to their previous levels within six and ten months, respectively. This was much faster than the pace we have seen markets recover historically. Not surprisingly, as prices recovered so did investor sentiment. But this enthusiasm was not prevalent amongst all asset classes. Two notable areas where investors still held widespread skepticism were Real Estate and Natural Resources. The common refrain around Natural Resources was that global demand would take years to recover with most commodities languishing as a result. For Real Estate, few believed the asset class could perform well in a world where offices were a relic of the past, retail shops were no longer needed, and much of the remaining physical real estate footprint would be rendered useless. Swings in sentiment this strong aren’t completely unheard of as investors are wired to extrapolate recent history. With this in mind, we made several changes to both asset classes last year, increasing our allocation to both, and came into 2021 with those two as our favorites to outperform. Through the first half of 2021 both asset class benchmarks are up 14% or more and are amongst the best performing asset classes. In this article, we’ll take a look at the primary drivers of this performance and offer an outlook for the second half of 2021.

Coming into 2020, Natural Resources was essentially a forgotten asset class. Many investors had written it off as it persistently lagged in the slower growth environment that has characterized the past decade. As COVID-19 wreaked havoc last spring, investors fled commodities, fearing that the global economy would soon be effectively shut down. With most workers at home, global supplies of commodities started to dry up with little work being done to replenish them. At the same time, we saw a wave of global fiscal and monetary stimulus that helped stabilize the global economy and spur demand. Despite mounting evidence of a global economic recovery late last year, rebuilding supply can be a lengthy process – particularly in more labor intensive commodities like copper or seasonal commodities like corn and soybeans. Against this backdrop of stagnant supply growth, numerous individual commodities saw significant rallies in late 2020, many of which have continued through the first half of 2021. The chart below shows two examples: copper (green line) and corn (purple line).

In the months after COVID-19 first hit, there were high levels of skepticism, uncertainty, and fear around the future of most investments, but Real Estate stood alone as the asset class where the prognosis was especially bleak. In April 2020, The New York Times wrote an article titled “The Death of the Department Store” while The Economist wrote a separate article, also in April, titled “Death of the Office”.1 Hyperbole, particularly during times of crises, is not unusual, but there was widespread concern around what the future would look like for most forms of real estate. Despite operating in an environment where uncertainty reigned, part of our conviction in real estate centered around the belief that even if conditions were worse than they were before COVID-19, most real estate investments were pricing in an overly dire outcome. Government intervention to support businesses prevented more substantial job loss and stimulus in the form of direct payments to individuals resulted in a 20% jump in the level of savings held at U.S. financial institutions during 2020. This led us to believe the consumer would be uncharacteristically healthy emerging from this recession. As vaccinations progressed in the first half of 2021, the worst-case scenario for Real Estate began to unravel. Workers started returning to offices, consumers returned en masse to retail stores and it slowly became clear that Real Estate would be just fine.

After a stellar first half of the year, our outlook for both Natural Resources and Real Estate remains upbeat, even if a touch more reserved versus the beginning of the year. As expectations rebounded, so have valuations and sentiment, leaving a more balanced risk-reward for both. Despite this, several tailwinds exist which support our positive outlook. First, global economic activity is still held back by COVID-19 in various parts of the world. As vaccinations progress, economic activity should recover helping both asset classes. Second, investor positioning has lagged other asset classes, especially in Real Estate, leaving room for investors to increase exposure, which could propel returns; low interest rates could incentivize investor flows into Real Estate to generate more income, for example. Lastly, with inflation atop of many investors’ minds, Real Estate and Natural Resources could benefit as investors position portfolios for potentially higher inflation as both asset classes have previously fared well in inflationary environments.

As Natural Resources and Real Estate go from forgotten to favored status, we remain on watch for exuberance, which tends to follow stretches of meaningful outperformance. Despite the benefit they have provided to client portfolios and our near-term optimism around the two asset classes, we won’t hesitate to trim exposure should the risk-reward deteriorate. In the meantime, we look forward to keeping you informed around developments in both asset classes, and the rest of your portfolio, as we move into the second half of 2021.

1 Catherine Nixey. “Death of the Office,” Published April 29, 2020, https://www.economist.com/1843/2020/04/29/death-of-the-office; Sapna Maheshwari, Vanessa Friedman. “The Death of the Department Store: ‘Very Few Are Likely to Survive’”, Published April 21, 2020, https://www.nytimes.com/2020/04/21/business/coronavirus-department-stores-neiman-marcus.html