Building wealth is a long-term endeavor. It takes discipline, foresight, and consistent effort. Yet, as much as we plan, unexpected risks can derail even the most well-structured financial strategy. A sudden health crisis, lawsuit, or economic shock can jeopardize decades of hard work. As Warren Buffett once said, “Building wealth isn’t about the number of smart decisions you make. It is about the number of mistakes you avoid.” The best way to avoid a mistake is to be prepared.

Let’s explore how to identify and prepare for the unexpected. The goal is not to live in fear of what could go wrong, but to build safeguards into your financial plan so you can weather the storms and stay on track toward your long-term vision.

The Nature of Unexpected Risks

Unexpected risks take many forms. Some strike suddenly—like an accident or a lawsuit. Others build silently over time, such as inflation eroding purchasing power or an overlooked liability that grows into a major problem. What they all share is unpredictability—an ability to disrupt your financial foundation if you are unprepared.

These risks often fall into four broad categories:

- Personal Risks – health crises, disability, premature death.

- Liability Risks – accidents or lawsuits.

- Market & Economic Risks – recessions, inflation, interest rate swings.

- Family & Legacy Risks – divorce, family disputes, inadequate estate planning.

By recognizing these categories, you begin to see the vulnerabilities in your plan—and the strategies available to protect yourself.

Risk #1: Personal Health

Health risks are among the most personal and unpredictable. A sudden illness or injury can lead not only to physical hardship but also to major financial strain.

Medical expenses—or the inability to earn an income—can quickly unravel a financial plan, and they happen more often than most people realize. An unexpected death can also leave loved ones not only emotionally devastated but financially vulnerable.

Strategies to Prepare:

- Disability Insurance: Roughly 1 in 4 workers will experience a disability lasting 90 days or more during their career. When it happens, it often lasts longer than expected—the average claim is nearly three years, and about 1 in 8 workers will be disabled for five years or more.1 Without income protection, savings erode quickly, making disability insurance a powerful safeguard for long-term security.

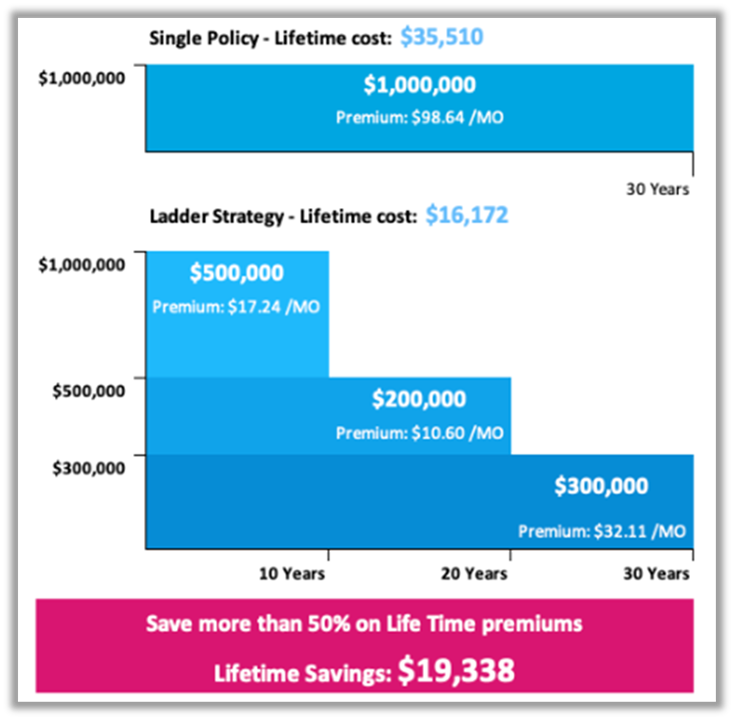

- Laddered Term Life Insurance: Many affluent individuals carry insufficient life insurance. A cost-effective solution is laddered term life insurance, which matches coverage to actual financial needs over time rather than locking into one large policy that may be unnecessary later. By layering policies with staggered end dates, you achieve cost savings as obligations decline—for example, as children become independent or a mortgage is paid off. This approach also provides flexibility, ensuring the right coverage during high-responsibility years without overpaying once major obligations have passed.

Source: PolicyAdvisor

Note: For more on laddered term life insurance and protecting yourself, see “Underinsured and Overlooked.”*

Affluent individuals often neglect disability and life insurance due to misconceptions about their financial security or the cost of coverage. Yet integrating these tools into a wealth plan closes a significant gap of risk for families and legacies.

Risk #2: Liability and Litigation

High-net-worth individuals are increasingly targets for lawsuits—whether from business dealings, auto accidents, or personal liability. A single claim could threaten your wealth if you are not adequately protected.

Many believe their existing homeowners or auto insurance provides enough protection, but these policies often fall short. For instance, assume someone has a $1 million auto liability policy and a $1 million umbrella policy. If they cause a fatal auto accident in an affluent neighborhood, the settlement could exceed $2 million—leaving them personally responsible for the difference.

Strategy to Prepare:

- Umbrella Liability Insurance: This coverage extends beyond the limits of primary policies (home, auto, rental, boat, etc.) and is surprisingly affordable. It is particularly important for individuals who own rental property, have teenage drivers, frequently host guests, or own swimming pools. While the odds of using umbrella insurance are low, as one wise man said, “Throw statistics out the window if it happens to you.”

Risk #3: Family and Legacy Disruptions

Money doesn’t exist in a vacuum—it’s tied to relationships. Unexpected family events, such as incapacity or disputes over inheritance, can erode wealth as quickly as market downturns.

Strategies to Prepare:

- Estate Planning: Wills, trusts, and powers of attorney ensure your intentions are clearly documented and legally enforceable, reducing uncertainty for loved ones. These tools minimize conflict by clarifying wishes, preventing disputes, and guiding families during difficult times.

- Clear Communication: Once an estate plan is executed, clear communication is equally important. Wills and trust documents should explicitly outline intentions for asset distribution, trustee responsibilities, and beneficiary provisions. Transparency and family conversations prevent misunderstandings and legal challenges that can arise from vague or incomplete instructions.

Note: For more on estate planning, see “Protecting Your Children After Your Passing.”*

One of the greatest risks to wealth is not external—it is family discord. Thoughtful planning and communication significantly reduce this risk.

Final Thoughts

Unexpected risks are, by definition, impossible to fully anticipate. But they are not impossible to prepare for. By recognizing risks—health, liability, and family dynamics—you take the first step toward resilience.

The strategies outlined here are not one-size-fits-all. Each wealth plan must be customized to reflect unique circumstances, values, and goals. That’s why ongoing review, thoughtful design, and clear communication are essential.

As Benjamin Franklin wisely put it, “By failing to prepare, you are preparing to fail.” In wealth management, preparation isn’t optional—it’s the cornerstone of protecting what you’ve built and ensuring it endures.

1 Source: Council for Disability Awareness