Entering 2023, the consensus outlook was bearish for most asset classes. Inflation would remain stubbornly high. Interest rates would continue to rise and remain higher for much longer. Corporate earnings would fall 5-10%, with many strategists calling for steeper declines. Finally, valuation multiples would contract as a result of lower earnings and higher interest rates.

However, 2023 became the year of inflections, with many investors finding themselves underperforming and scrambling to chase benchmarks toward the end of the year. Inflation moderated, interest rates are now expected to be lower in 2024, corporate earnings were flat, and multiples expanded. The inflections were so significant that multiple asset classes entered November with year-to-date losses only to end the year with full year gains.

How did these inflections play out and what do they mean for 2024?

The inflections can be summarized in four parts.

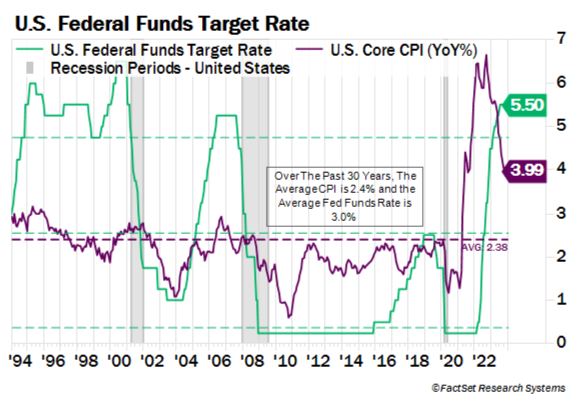

The first domino fell when inflation started to plummet in the spring. After reaching a peak of 6.64% in 2022, Core CPI started 2023 at 5.70%. By the end of 2023, Core CPI was below 4%. Investors underestimated the speed at which inflation was able to normalize. At Osborne Partners, we positioned your portfolio for a steep drop in inflation in the fall of 2022, as numerous forward-looking metrics were indicating tame future inflation.

The inflation inflection caused the second main inflection: the Fed stopped raising short-term interest rates. This caused longer-term interest rates to peak. After touching 5% in the second half of 2023, the 10-year U.S. Treasury yield started and finished the year at literally the same level – just below 3.9%. The black line shows the 2023 starting and ending yields. As rates were peaking in the summer and fall, the Investment Team purchased more individual bonds in a four-month period than we had over the previous 15 years.

Inflection point number three was corporate earnings. As inflation fell faster than expected and interest rates peaked, corporations were helped in multiple ways. Falling inflation helped maintain profit margins while falling interest rates reduced borrowing costs. The combination of the two improved business and consumer confidence. In the end, the dire expectations for plummeting corporate earnings were well off the mark, as earnings were essentially flat for the year and growth rates bottomed in August.

The final, and arguably most important inflection came in the form of valuation multiples. How does the S&P 500 rise over 25% when earnings are flat? The P/E multiple rises 25%.

Although the earnings multiple started the year at 17.8x and rose to over 22x in the summer, by the end of October, the S&P 500 P/E on trailing earnings had deflated to 20x. At this point, the S&P 500 was up about 7% for the year and investor sentiment was negative.

However, once the surprisingly decent third quarter earnings were digested, and the October Core CPI release showed a sixth month in a row of slowing inflation, it was clear the Fed was likely finished with their hiking cycle. Once investors realized the Fed Funds rate was 150 basis points above inflation, which was continuing to fall, a rally in risk assets like equities began.

Many of the strongest and most successful equities rallies catch the too bearish consensus off-guard. This one was no exception. Domestic equities, which were up about 7% in late October, finished the year up over 25%. Meanwhile, valuation multiples ended 2023 above 22x.

To make the environment worse for investors, the full year returns were quite narrow. Over 70% of companies in the S&P 500 underperformed the overall index. More broadly, 8 out of 11 entire sectors underperformed the S&P 500. Essentially the performance of three sectors were 90% of the total return.

Foreign equities that were down for the year in late October, finished up 15% for 2023. The real estate asset class, which also posted a negative year through October, ended the year up 9%. The average hedge fund that was overly hedged and very bearish in the fall posted a 7% gain (HFRI Hedge Fund Index). Fixed income, depending on the sub-group, rose 4-5% during the interest rate whipsaw. Only the natural resources asset class fell during the year, losing 8% mainly due to the trajectory of inflation.

What does this mean for 2024 prospects?

First, although Osborne Partners once again outperformed in each asset class versus benchmarks, we do not expect similar gains in 2024. In previewing our asset class stoplight for 2024, there are three shifts versus the start of the 2023 – domestic equities, natural resources, and real estate.

At the start of 2023, we believed domestic equities had a three-pronged opportunity to outperform. Valuation multiples were tame, earnings estimates were moderately negative, and sentiment was negative. Our list of high reward-to-risk opportunities was one of the lengthiest over the past decade. Today, valuation multiples are above average (a mild negative), earnings estimates have bottomed (a positive), and sentiment has become overly bullish (a negative). As we enter 2024, one positive in our positioning is the majority of the S&P 500’s overvaluation stems from the ten largest companies and the five largest consumer staples companies. These 15 companies combined represent a whopping 36% of the index. Our exposure to this overvalued pocket of the S&P 500 is only 18%.

We continue to find a number of strong opportunities in foreign equities. Our allocation is shifting toward individual companies and away from macro country exposure. With the S&P 500 now trading at a multi-decade record premium of 50% to the rest of the world, the risk-reward is simply superior outside the U.S. The overwhelming majority of investors are underweight foreign equities, with many simply having no exposure whatsoever.

After shifting to a neutral stance in late 2022, we are now underweight natural resources. Until inflation troughs and/or we unearth a special situation or two, we will continue to be underweight.

Our solid returns and neutral positioning in real estate ended with our complete sale of our homebuilding position. While REITs are beginning to show signs of a fundamental trough, and interest rate differentials are improving, this is an asset class where our underweight continues. We have fielded a number of client inquiries about when our alternatives strategy will revert to hedging from capital appreciation. While our alternatives returns were strong in 2023, we find our holdings offering a good risk-reward as 2024 begins.

In fixed income, after completing a record individual bond buying spree over the summer and fall of 2023, we continue to see the opportunity to increase overall portfolio yields as shorter-maturity bonds purchased in 2019-2022 mature in our portfolios.

Finally, regardless of our portfolio returns year-to-year, as a team we always analyze the prior year to find lessons to be learned, and ways to continually improve our discipline. Last year was a year of psychology and expectations. As a team, I believe one of our strengths is we understand investing psychology well. “Group think” is pervasive throughout our industry. This phenomenon causes sentiment extremes that are many times derived from emotions versus fact. Every day we strive to perform deep analysis, pay close attention to valuation, be style-agnostic, and always understand psychology. Instead of “drowning out the noise and emotions”, we try to take advantage of it.

Understanding expectations helps in investing as well. Why will a stock obliterate an earnings estimate, yet trade down, while another misses earnings estimates, but trades higher? It is our job to attempt to gauge expectations. Expectations and reactions can indicate whether our thesis is playing out correctly or not. Layer on the fact that investments tend to move 6-12 months in advance of fundamentals, and it is easy to understand why our job is both fulfilling and frustrating.

The good news is we enjoy the frustration and fulfilling nature of our job. The bad news is 2024 will inevitably be a year of both.